The impact of tax reform on the dental industry

With the passing of The Tax Cuts and Jobs Act (TCJA) in December 2017, there have been significant changes in tax law, the majority of which are effective for the 2018 tax year. This is part one in a four-part series on the most significant changes in tax law that will impact the dental industry, considerations for practices and individual tax situations for dentists.

Individuals

Outlined below are some of the key changes affecting individuals and considerations to be aware of when planning.

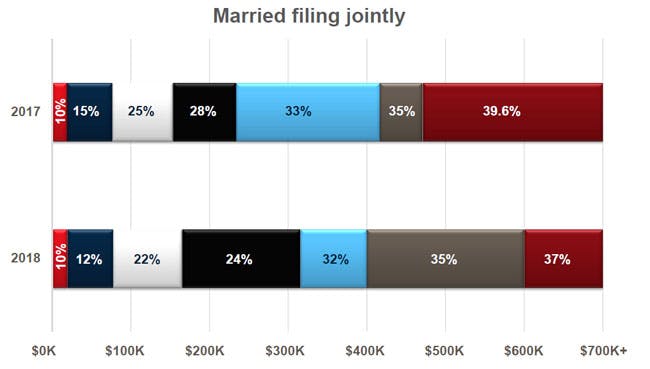

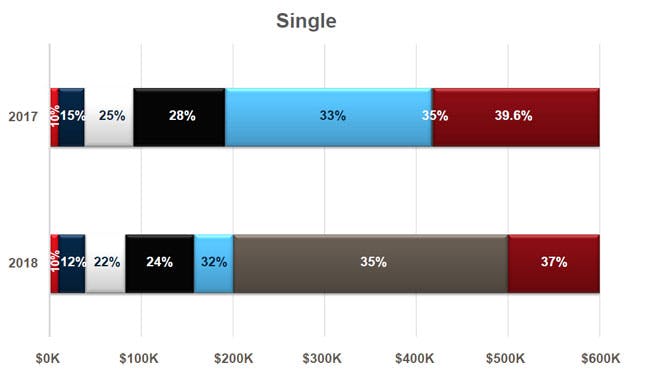

The two most significant changes to the tax bracket for both married filing jointly and single taxpayers are in the reduction of the top rate to 37 percent from 39.6 percent and the general widening of each tax bracket (graphs below).

The alternative minimum tax (AMT) saw a change with the increase of the exemption amount and phase-out thresholds. This will likely result in far fewer taxpayers being subject to AMT in 2018 and beyond. The new limitations of the state and local tax deduction will also lead to fewer taxpayers being subject to AMT.

The standard deduction was doubled for married filing jointly taxpayers to $24,000 and single taxpayers to $12,000. As a result of this change, personal exemptions are suspended until 2026. In addition, other changes to itemized deductions include suspending the following items until 2026:

- Real estate and state income tax deductions are limited to $10,000

- Mortgage interest deductions are limited to interest incurred on indebtedness of $750,000 for debt incurred after Dec. 31, 2017; home equity interest is now disallowed

- Miscellaneous itemized deductions, including unreimbursed employee business expenses and investment advisory fees, were eliminated

As for estate-planning considerations, alimony is no longer deductible for divorce/separation agreements finalized after 2018, and the estate tax limit doubled to approximately $11 million per individual. Additionally, the child tax credit was doubled to $2,000 and the income phase-out for the credit now begins at $200,000 for single taxpayers and $400,000 for married taxpayers.

General considerations for dental practices

The Domestic Production Activities Deduction (DPAD) for in-house manufacturing of crowns and other restorations was eliminated.

Several changes were made to depreciation rules, the majority of which are favorable for taxpayers, including:

- Bonus depreciation rules now allow for 100 percent bonus depreciation and inclusion of used assets with a depreciable life of 20 years or less

- Up to $1 million of section 179 depreciation can be claimed (previously $500,000); however, it is subject to limitations

- Section 179 depreciation can now be used on some nonresidential real estate improvements (qualified improvement property)

- Adjustments to vehicle depreciation limits

- Generally expires for assets acquired and placed in service after Dec. 31, 2026

The changes above increase the benefits of a cost segregation study, which is an in-depth analysis of the costs associated with the construction, acquisition or renovation of owned or leased buildings and can identify assets eligible for shorter tax recovery periods, rather than real property periods (typically 39 years). Read more on the changes to bonus depreciation rules, recovery periods for real property and expanded section 179 expensing.

Entertainment expenses are no longer deductible, and meals with a business purpose remain 50 percent deductible.

The TCJA created a new general business tax credit for employers that voluntarily offer more than two weeks of paid family and medical leave annually to qualifying employees if the employer pays more than 50 percent of an employee’s wage during their leave.

Pass-through entities (S corporations and partnerships)

One of the most asked about topics is the new qualified business income (QBI) deduction on domestic income that is available to pass-through entities and sole proprietorships. The deduction is calculated as a 20 percent reduction of income generated by a trade or business and is subject to the following limitations:

- The greater of 50 percent of wages, or 25 percent of wages plus 2.5 percent of the unadjusted basis of property

- Taxable income in excess of $315,000 for married taxpayers and $157,500 for single taxpayers. The deduction is reduced to zero when taxable income exceeds $415,000 (married) or $207,500 (single) for specified service businesses including dental and medical practices

The deduction is currently set to expire after 2025 and effectively reduces the top tax rate to 29.6 percent from 37 percent on income from a trade or business.

C corporations

The corporate tax rate was reduced to a flat 21 percent for tax years beginning after Dec. 31, 2017, which is the same rate for personal service corporations. Previously, the highest rate was 35 percent.

The reduction in corporate rates has led to a lot of questions regarding corporate structure and whether a practice should remain a pass-through entity or become a C corporation. When determining the best approach for your dental practice, various factors should be taken into consideration other than simply looking at the rate differential between individuals and corporations, including:

- Double tax on C corporations (which for most may make the corporate effective rate still higher than the single tax rate of S corporations) or partnership tax (LLC)

- State income taxes are deductible for corporations and limited for individuals

- Plans for after-tax cash flow, including leaving in the corporation to grow and pay down debt or distribute excess cash to owners

- Time horizon for operating the business

- The owner’s exit strategy

- Impact of net investment income tax

- Employee considerations – including wages and fringe benefits

- Permanency of current tax rates

- C corporations are not eligible for the QBI deduction

Next steps

Dental practices should contact their advisor earlier in the year as tax planning will be more in-depth for 2018. When discussing how to maximize tax savings and planning opportunities in 2018, dental practices should consider the following:

- Estimating charitable contributions

- Deferring paying real estate taxes until due

- Maximizing IRA (or other retirement plan) contributions and HSA contributions (if covered by a high-deductible health plan)

- Evaluating benefits of 529 savings plan for education expenses for dependents

- Checking your withholding and quarterly estimated tax payments

- Evaluating meals and entertainment expenses under reduced tax benefits and update accounting records for changes

- Properly planning accelerated depreciation and evaluate benefits of cost segregation study

- Determining whether you qualify for the Credit for Paid Family and Medical Leave

- Considering how to maximize the 20 percent QBI deduction

- Evaluating entity choice

Subscribe to the Dental Bites newsletter

For more information on this topic, or to learn how Baker Tilly dental practice specialists can help, contact our team.

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.