SSAP No. 101 update and Q&A observations: Admissibility calculation

Continued from SSAP No. 101 update and Q&A observations: Statutory valuation allowance

Admissibility calculation

The admissibility calculation under SSAP No. 101 admits adjusted gross deferred tax assets (gross deferred tax assets less applicable statutory valuation allowance) based upon a three-component admission calculation in an amount equal to the sum of paragraphs 11.a., 11.b., and 11.c. SSAP No. 10R also admitted adjusted gross deferred tax assets under a three-component admission calculation under paragraphs 10.a., 10.b., and 10.c. However, under SSAP No. 10R, reporting entities could elect increased admissibility under paragraph 10.d. if certain risk-based capital criterion were met, and include paragraph 10.e. as part of the admissibility calculation. There is no such election under SSAP No. 101. The admissibility calculation is performed on a separate company, reporting entity basis.

Paragraph 11.a.

Paragraph 11.a. of SSAP No. 101 admits adjusted gross deferred tax assets equal to the amount of federal income taxes paid in prior years that can be recovered through loss carrybacks for existing temporary differences that reverse during a timeframe corresponding with IRS tax loss carryback provisions, not to exceed three years. Therefore, SSAP No. 101 is more in line with what happens on a reporting entity’s tax return, as it admits adjusted gross deferred tax assets based upon IRS tax loss carryback provisions. This component of the admissibility calculation is entity specific, as a life entity has a three year carryback period for ordinary losses and capital losses, whereas a non-life entity has a two year carryback period for ordinary losses and a three year carryback for capital losses.

The amount of federal taxes paid includes taxes that were or will be reported on the reporting entity’s federal income tax return for the periods included in the carryback period. This includes both regular tax and alternative minimum tax, but does not include any interest or penalties that may be included on the tax return. It also includes tax loss contingencies established in accordance with the provision of SSAP No. 5R. SSAP No. 101 clarifies that a reporting entity that files a consolidated federal income tax return with its parent should look to the amount of taxes it paid (or were allocated to it) as a separate legal entity in determining the admitted deferred tax asset under paragraph 11.a. It is also limited to the amount that the reporting entity could reasonably expect to have refunded by its parent.

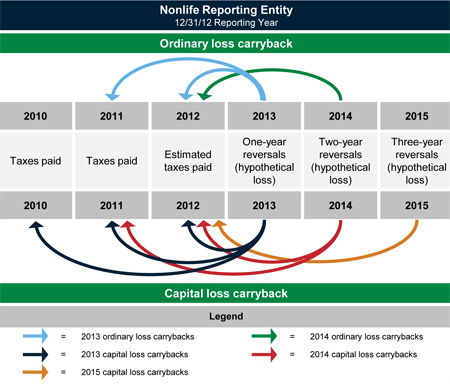

Q&A observations

The Q&A provides several important clarifications related to the first component of the admissibility calculation. It introduces the concept of a "hypothetical loss" by stating that a reporting entity should treat existing temporary differences that reverse during a timeframe corresponding with IRS tax loss carryback provisions as ordinary or capital losses that originated in each such subsequent year. More importantly, it clarifies that the reversing temporary differences (hypothetical losses) are specific to each year in which they reverse, and in turn, to the specific year(s) to which they can be carried back corresponding with IRS tax loss carryback provisions. This is similar to how a reporting entity would file a Form 1139, Corporation Application for Tentative Refund.

In addition, if the hypothetical loss carrybacks trigger the alternative minimum tax, taxes recoverable in the carryback years may be limited. This first component of the admissibility calculation is available to all entities, regardless of whether or not certain threshold limitations are met under the second component of the admissibility calculation, or paragraph 11.b.

Paragraph 11.b.

Paragraph 11.b. of SSAP No. 101 admits adjusted gross deferred tax assets equal to the lesser of the following:

- 11.b.i. – The amount of adjusted gross deferred tax assets, after the application of paragraph 11.a., expected to be realized within the applicable period following the balance sheet date; or

- 11.b.ii. – An amount that is no greater than the applicable percentage of statutory capital and surplus as required to be shown on the statutory balance sheet for the current period.

This component of SSAP No. 101 introduces the concept of Realization Threshold Limitation Tables. The Realization Threshold Limitation Tables are specific to the following types of reporting entities:

- RBC Reporting Entities

- Financial Guaranty or Mortgage Guaranty Non-RBC Reporting Entities

- Other Non-RBC Reporting Entities

A reporting entity admits adjusted gross deferred tax assets under 11.b.i. and 11.b.ii. based upon where they fall on their applicable Realization Threshold Limitation Table.

Realization Threshold Limitation Table – RBC Reporting Entities

ExDTA ACL RBC (%)*

11.b.i.

11.b.ii.

Greater than 300%

3 years

15%

200 – 300%

1 year

10%

Less than 200%

0 years

0%

* The December 31 Risk-Based Capital ratio is calculated based on the Authorized Control Level RBC filed with the state of domicile and computed without net deferred tax assets.

This component of the admissibility calculation requires a reporting entity to determine the realization of reversing temporary differences based upon a "with and without" calculation. The "with and without" calculation determines the tax savings of reversing temporary differences by calculating the tax liability on projected taxable income in the applicable periods both with reversing temporary differences and without reversing temporary differences. The reversing temporary differences must be consistent with the reversal patterns as determined under paragraph 11.a. of the admissibility calculation.

The reporting entity must estimate its projected separate company taxable income and the tax benefit that it expects to receive from reversing deductible temporary differences in the form of lower tax payments to its parent. A reporting entity that projects a tax loss in the applicable realization period cannot admit a deferred tax asset related to the loss under paragraph 11.b., even if the loss could offset taxable income of other members in the consolidated group and the reporting entity could expect to be paid for the tax benefit pursuant to its tax allocation agreement.

Q&A observations

While the change to using current period capital and surplus under paragraph 11.b. of SSAP No. 101 may result in increased difficulty, the Q&A outlines administrative ease if a reporting entity’s surplus is increasing. The phrase "an amount that is no greater than" under paragraph 11.b.ii. allows an entity to utilize an amount lower than what would be allowed if it utilized the amount of statutory capital and surplus as required to be shown on the statutory balance sheet of the reporting entity for the current period’s statement. For example, the reporting entity could utilize the amount of statutory capital and surplus from the most recently filed statement. Also, in the event that late immaterial modifications to a reporting entity’s statutory financial statements occur subsequent to initial completion of the statutory financial statements but prior to filing, these immaterial changes do not need to be reflected in the footnotes, if such modifications do not cause the reporting entity to change the threshold limitation from the applicable Realization Threshold Limitation Table.

The Q&A also provides additional clarification related to the projection of taxable income for use in the "with and without" calculations under paragraph 11.b.i. Future originating differences, and their subsequent reversals, are considered in assessing the existence of future taxable income. However, future originating differences should not impact the scheduling of existing temporary difference reversals during the applicable period. The reversing existing temporary differences used under paragraph 11.b. should mirror the reversals of existing temporary differences under paragraph 11.a.

Paragraph 11.c.

Paragraph 11.c. of SSAP No. 101 admits adjusted gross deferred tax assets, after application of paragraphs 11.a. and 11.b., which can be offset against existing gross deferred tax liabilities. The reporting entity shall consider the character of the deferred tax assets and deferred tax liabilities such that offsetting would be permitted in the tax return under existing enacted federal income tax laws and regulations. The reporting entity shall also consider the reversal pattern of the temporary differences, but not beyond that required for the statutory valuation allowance under paragraph 7.e.

Q&A observations

When considering the offset of gross deferred tax assets against gross deferred tax liabilities, the character must be considered. For example, an adjusted gross deferred tax asset related to unrealized capital losses cannot be offset against an ordinary deferred tax liability. This is because a capital loss cannot offset ordinary income on a reporting entity’s tax return. However, an ordinary gross deferred tax asset can be admitted by an offset with an ordinary deferred tax liability or a capital deferred tax liability. An ordinary loss can be offset by a capital gain on a reporting entity’s tax return.

Scheduling is required under this component of the admissibility calculation, to the extent it is required in the determination of the statutory valuation allowance. If a scheduling exercise was performed when determining the amount of a statutory valuation allowance, the scheduling should be consistent under paragraph 11.c. Even if scheduling was not required under paragraph 7.e., a reporting entity should still consider the reversal pattern of gross deferred tax liabilities and gross deferred tax assets. For example, an entity that has an indefinite lived intangible should not consider that deferred tax liability as a possible offset against reversing gross deferred tax assets.