Article

SECURE 2.0: Optional changes for 401(k) plans

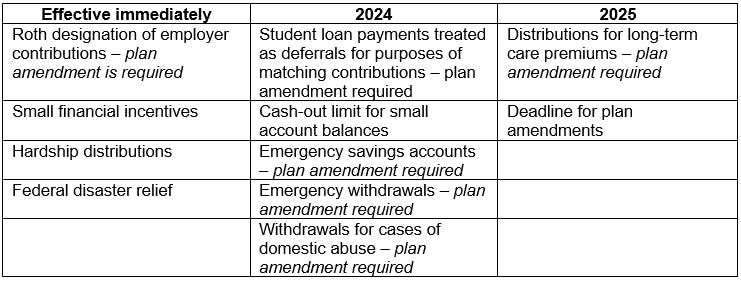

Summary of optional provisions

Explanation of optional provisions

1. Provisions effective immediately

Roth designation of employer contributions

Prior to SECURE 2.0, employer matching or non-elective contributions to a 401(k) plan were required to be made on a pretax basis. However, SECURE 2.0 provides plan participants with the ability to elect to receive matching contributions and non-elective contributions on an after-tax Roth basis. Roth employer contributions are taxable to the employee when made. In addition, participants must be 100% vested at the time the contribution is made. If non-Roth employer contributions vest over a period of time, it could result in an employer maintaining multiple vesting schedules. The plan’s record keeper and payroll provider should be consulted to ensure the employer contributions are recorded correctly. Since SECURE 2.0 does not address how a Roth-designate employer contribution should be reported for tax purposes, e.g., Form W-2 or Form 1099-R, guidance from the IRS is anticipated. If an employer chooses to add this provision to its plan, a plan amendment is required.

Small financial incentives

Another optional provision in SECURE 2.0 permits an employer to offer de minimis financial incentives to encourage employees to make salary deferral contributions to a 401(k) plan. Previously, financial incentives that could be provided by an employer were limited to matching contributions. Although SECURE 2.0 specifies that an employer may not use plan assets to provide financial incentives, it does not define what constitutes a de minimis financial incentive. It is anticipated that the IRS will provide guidance. This provision does not require a plan amendment.

Hardship distributions

Pursuant to SECURE 2.0, an employer with a 401(k) plan that permits distributions on account of hardship can rely on the employee’s certification that the employee had an event that meets the deemed hardship criteria. Previously, the employer’s reliance on the employee’s self-certification was limited to the amount needed to satisfy the hardship. Self-certification applies to plan years beginning after Dec. 29, 2022.

Federal disaster relief

Prior to SECURE 2.0 and subject to congressional action, a participant in a 401(k) plan could request a distribution in the event of a federally declared disaster as was provided in the Coronavirus Aid, Relief and Economic Security (CARES) Act. SECURE 2.0 makes such distributions permanent. Distributions are limited to $22,000 per disaster and are not subject to the 10% early distribution tax. They are included in income over a period of three years for income tax purposes and may be repaid to the plan during the three years. In addition, SECURE 2.0 increases participant loan limits in connection with a federally declared disaster to the lesser of $100,000 or 50% of the participant’s vested account balance and extends the repayment terms.

2. Provisions effective in 2024

Student loan payments treated as deferrals for purposes of matching contributions

SECURE 2.0 permits employers to make matching contributions under a 401(k) plan with respect to qualified student loan payments as though those payments were elective deferrals. A qualified student loan payment is defined as any indebtedness incurred by the employee solely to pay qualified higher education expenses of the employee. The employee is required to certify to the employer that the employee actually made the student loan payment; the employer may rely on the employee’s certification. Qualified student loan payments made by the employee could be matched up to the annual elective deferral threshold. This provision requires a plan amendment.

Cash-out limit for small account balances

SECURE 2.0 increases the involuntary cash-out limit to $7,000 from $5,000 for former employees. By cashing out accounts of former employees with small balances, administrative costs may be reduced and the employer does not have to track former employees.

Emergency savings accounts

SECURE 2.0 permits employers to add emergency savings accounts to their 401(k) plans. The emergency savings account is limited to nonhighly compensated employees and has a maximum contribution limit of $2,500. The employer may set it up with automatic enrollment at no more than 3% of pay, or may make it available to participants who choose to fund it. Participant contributions are treated as after-tax Roth contributions. Participants may make up to four withdrawals per year without incurring a fee. Given the complexity of this provision, it may be preferable to delay implementation until the IRS issues guidance. If an employer chooses to include emergency savings accounts, the plan should be amended.

Emergency withdrawals

SECURE 2.0 allows a participant in a 401(k) plan to take an emergency withdrawal to cover unforeseeable or immediate financial needs. The emergency withdrawal is limited to $1,000 and may be taken only once during the year. It is not subject to the additional 10% tax that applies to early distributions. Participants may repay the distribution within three years. If the participant chooses not to repay the distribution, the participant is not allowed to take another emergency withdrawal for three years. The plan should be amended if an employer chooses to permit emergency withdrawals.

Withdrawals for cases of domestic abuse

SECURE 2.0 also permits penalty-free distributions for survivors of domestic abuse. The amount that may be withdrawn is the lesser of $10,000 or 50% of the participant’s vested account balance. Participants may repay the distribution within three years. The plan should be amended if an employer chooses to permit emergency withdrawals.

3. Provisions effective in 2025

Distributions for long-term care premiums

SECURE 2.0 permits 401(k) plans to make distributions to participants for paying insurance premiums for long-term care. The maximum amount per year is $2,500 and is not subject to the early distribution tax of 10%. This provision requires a plan amendment.

Deadline for plan amendments

The timing for retirement plan amendments made pursuant to SECURE 2.0 is on or before the last day of the first plan year beginning on or after Jan. 1, 2025; governmental plans have until 2027. Although the deadline for plan amendments is not for two years, plans must be operationally compliant with required provisions and any optional provisions that are implemented.

To learn more about SECURE 2.0 and how these optional changes to 401(k) plans may affect you, please contact your Baker Tilly advisor.

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.